Last updated on September 2nd, 2024 at 07:40 pm

Last Updated on September 2, 2024 by

Consider financing your property using a wraparound mortgage when you want the highest price for your home in a high-interest rate market. What is a wraparound mortgage? Simple, it’s a form of seller financing. Your real estate agent lists your property indicating owner financing.

Your offer to finance will attract buyers with less-than-perfect credit or have a variety of other issues that prohibit the use of traditional mortgage options. The buyer agrees to your price and you sell just like any other type of sale except that the original mortgage is not paid off.

This is a short example: You have an existing first mortgage of $200,000. You are selling your house for $300,000. The buyer gives you a down payment of X which will be discussed later. The amount to be financed then is based upon amortizing the loan for 30 years.

Most owner financing using a wraparound mortgage loan includes a balloon payment due in three or five years. The purpose of a wraparound mortgage is to help the buyer get into your house until their credit or other situation improves. A short term of three to five years is usually satisfactory.

Reasons for a Home Seller to Offer a WrapAround Mortgage

A wrap-around mortgage can offer several advantages to a home seller. Here are some key reasons:

- Higher Interest Rate: Sellers can often set a higher interest rate on a wrap-around mortgage compared to the rate on their existing loan. This can generate additional income on the property.

- Tax Benefits: In some cases, the seller may be able to defer capital gains taxes on the sale of the property by using a wrap-around mortgage.

- Continued Income: The seller continues to receive monthly mortgage payments, providing a steady stream of income.

- Retained Equity: If the seller retains a portion of the equity in the property, they can benefit from any appreciation in value.

- Flexibility in Terms: The seller has more flexibility in setting the terms of the wrap-around mortgage, such as the interest rate, repayment schedule, and prepayment penalties.

- Potential for Future Sale: If the buyer defaults on the wrap-around mortgage, the seller may be able to repossess the property and sell it again.

- Easier Sale: In some cases, a wraparound mortgage can make a property more attractive to buyers, especially those with credit challenges or limited down payment funds.

- Fast closing: Closing can take place within days of signing the purchase contract. The wait caused by the financing process has been eliminated.

- Pre-foreclosure: If a seller is losing the house e.g. early stages of foreclosure, the seller can use the buyer’s down payment to bring the mortgage up to date.

Reasons a Home Buyer Might Want a WrapAround Mortgage

A wrap-around mortgage can be a creative financing option for home buyers, especially in certain circumstances. Here are some reasons why a buyer might consider this type of arrangement:

- Easier Qualification: Wrap-around mortgages often have more flexible qualification criteria than traditional mortgages. This can be beneficial for buyers with less-than-perfect credit or limited income.

- Lower Closing Costs: Because there’s no need to involve a traditional lender, closing costs associated with a wrap-around mortgage can be lower.

- Higher Purchase Price: A wrap-around mortgage can sometimes allow a buyer to purchase a more expensive property than they could with traditional financing.

- Potential for Lower Interest Rates: In certain market conditions, the interest rate on a wrap-around mortgage might be lower than what’s available through traditional lenders.

- Flexibility: Wrap-around mortgages can offer more flexibility in terms of payment schedules and prepayment options.

- Seller Financing: If the seller is willing to offer financing, a wrap-around mortgage can be a way to avoid the traditional mortgage application process.

Now for the tricky part, let’s hit this head-on. Your lender has a “due-on-sale” clause in the existing loan. This means if you sell it, you must pay off the mortgage. In the example above, you have decided to sell the property anyway and continue making payments on the original loan. There will be a risk that if the seller’s mortgage holder learns of the sale they may call the loan due. This would create an issue.

Typical “due-on-sale” clause

“If all or any part of the property herein is transferred without the lender’s prior written consent, the lender may, at its option, require all sums secured hereby immediately due and payable.”

There are alternatives

The seller can pay off the first mortgage if they have the funds. An alternative is that the buyer is in a position to obtain a residential real estate loan and pay off the seller’s mortgage. Another possibility is that the buyer can agree to transfer the property back to the seller and the seller can notify the lender the property is now in their name.

Regardless of the results of this call for the note, one or more of the above are solutions. More often the lender is not aware of the transfer of ownership. Many people transfer their property to an LLC. This is a technical violation of the due-on-sale clause and the buyer’s mortgage is not affected.

A closing attorney can work out the language for the “what happens if” scenario in advance and include it in the terms of the loan. Remember this is a temporary loan that works for both parties. Now for the other details of the loan.

In the event, the Original Mortgage Company Calls the Seller’s Note

If the seller’s mortgage company calls the note, both the buyer and seller must agree on the steps to take. In such a situation, the seller will immediately notify the buyer.

A resolution may require the involvement of an attorney to create and document a suitable plan. Here are some potential options, but not all:

- Buyer Pays Off Seller: The buyer pays off the entire loan to the seller, who then uses those funds to pay off the original mortgage.

- Seller Pays Off Original Mortgage: The seller may be able to pay off the original mortgage directly, potentially renegotiating the terms with the lender.

- Conversion to Lease to Buy: The purchase may be converted into a lease-to-buy agreement, with credit given to the buyer for the down payment and any equity payments made to date.

Pre-Foreclosure

The seller may be in the early stages of foreclosure. The mortgage company will start the process after the mortgage payment is greater than 30 days late (depending upon the purchase contract). The mortgagor or seller in this case usually has up to an additional 60 days to bring the mortgage current. During that period, the seller can sign a contract for the sale with a buyer and use the buyer’s deposit to cure the mortgage.

Years ago, I was buying a multi-family property, and about two weeks into the process the seller told me that she had one week before foreclosure. This purchase was to be financed and there was no time to close the loan before the lender foreclosed. The only way for her to save her property was to initiate a wraparound mortgage immediately. Within the week the deal was closed.

Pre-foreclosure may be the most common use of wraparound mortgage financing. It’s often used as an emergency fix.

There may be additional options to consider. Working with a real estate attorney may solve any open issues.

The buyer

Your listing agent will receive an offer from another real estate agent representing the buyer or the buyer may come to your agent directly. Since you the buyer are the lender, you need to gather information about the buyer. One good source to obtain a credit score and background information can be found here

The interest rate

As a seller financing their property, you can set the interest rate. These types of loans are higher risk and with that higher risk comes higher interest rates. At the time of this writing, a 720 credit score with a 20% down payment would result in a 6.75% interest for a 30-year amortized loan. It is unlikely that your buyer will have a 720 credit score or 20% down. This ratchets up the interest rate to 8% to 10% APR. 10% would be more common showing a 3.25% premium.

You have options about the interest rate and the price of the house. If you were selling it for $300,000 and the average buyer with their financing option would probably pay about $290,000, you know that seller financing will gain a higher selling price.

You can gain a higher selling price because the buyer can not obtain traditional financing nor can they make a traditional down payment. If the buyer has trouble with the payment as you have it structured, you could lower the interest rate for the first year. Essentially it’s like you have bought down the interest rate for them.

You keep the difference in interest rates

The actual interest rate in the first mortgage that the seller is paying will probably be lower than 10% probably in the area of 4%-6%. The difference between for example 5% the seller is paying and 10% the buyer is paying will produce additional income to the property seller.

As mentioned a traditional mortgage loan can require from 3.5% up as a down payment. Most conventional mortgage loans require 20% down to avoid PMI or MIP. With the mortgage wrap, the down payment is entirely up to the seller. Consider your costs as a seller.

You the seller, will be responsible for a real estate commission on one side (the seller’s commission) and a few hundred dollars for closing costs. As an example, you pay 2.7% of $300,000 to your real estate agent which is $8,100. You would want at least 5% down or $15,000. This would leave you with about $6,400. It would be best to place these funds into a savings account for “just in case”.

Should the buyer be represented by a real estate agent, you would be responsible for negotiating the buyer’s agent commission. New rules are in place regarding the payment of commissions to any real estate agents. You may have costs of $16,200 using the numbers above. In this case, you can either pay the real estate agent commission from your own funds or increase the down payment to cover the closing costs and real estate fees.

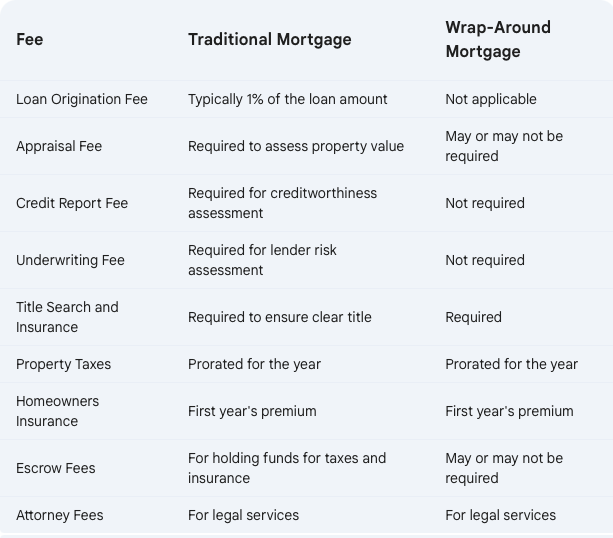

Closing costs – Traditional vs Wraparound Mortgage

About closing costs. This is another key reason that buyers may want to avoid a conventional loan. Those financing costs which can be substantial don’t exist in wraparound transactions. This can save the buyer thousands of dollars. The loan will go to a real closing but the costs will be limited to a title insurance fee, escrow/attorneys closing fees, and other minor costs.

A wraparound mortgage loan will require that homeowners insurance and property taxes are addressed. The way to do this is to have the buyer pay principal, interest for the loan plus the seller’s insurance and property tax. The sellers are paying $200 per month into escrow for property tax and $250 into escrow for homeowners insurance. The buyer will pay $450 per month in addition to the principal and interest on their loan.

Keeping the existing situation with homeowners insurance and property taxes under the seller helps to protect the seller’s interest. How can the buyer benefit from this arrangement?

The buyer will pay the seller’s first mortgage directly to the mortgage company. The best way for this to occur is for the buyer to set up a bill pay account with their bank for the amount of the total mortgage payment with taxes and insurance each month. This means that no one forgets to send the check, it goes automatically. If for some reason this does not work, the seller can mail the payment using the seller’s return address.

Example of the wraparound mortgage loan breakdown

Here is a table showing a home buyer paying $300,000 for a house with a 5% down payment and a 30-year amortized loan at 9% interest.

Assumptions:

- Home Price: $300,000

- Down Payment: 5% of $300,000 = $15,000

- Loan Amount: $300,000 – $15,000 = $285,000

- Interest Rate: 9% annually

- Loan Term: 30 years (360 months)

Monthly Mortgage Payment Calculation:

The monthly mortgage payment for a $285,000 loan at a 9% interest rate over 30 years would be approximately $2,293.17.

Here is a breakdown of the home purchase and wraparound mortgage details:

| Description | Amount |

|---|---|

| Home Price | $300,000 |

| Down Payment (5%) | $15,000 |

| Loan Amount | $285,000 |

| Interest Rate (Annual) | 9% |

| Loan Term | 30 years |

| Monthly Mortgage Payment | $2,293.17 |

Here’s the table that breaks down the two payments the buyer will make, with one payment to the mortgage company and the second payment directly to the seller:

| Description | Amount |

|---|---|

| Total Monthly Mortgage Payment | $2,293.17 |

| Payment 1 (to Mortgage Company) | $1,193.00 |

| Payment 2 (to Seller for Equity Loan) | $1,100.17 |

Explanation:

- Total Monthly Mortgage Payment: The buyer’s total monthly payment is $2,293.17.

- Payment 1 (to Mortgage Company): The buyer pays $1,193.00 to cover the seller’s existing mortgage.

- Payment 2 (to Seller): The buyer also pays $1,100.17 directly to the seller to cover the equity loan of $85,000 at 9% interest over 30 years.

This setup keeps the total monthly payment consistent with the original mortgage calculation of $2,293.17 while dividing the payments between the mortgage company and the seller. Let me know if you need further details or adjustments!

Both parties can be fully informed of the transactions if the seller grants the buyer access to their mortgage loan account online or at minimum sends a copy of the monthly statement by email each month showing the payment being made. The seller will use the mortgage statement which comes to them to track the payment progress along with internet access.

Key documents required

The closing attorney will prepare two key documents. The first is shown below, a note. The note explains how much is owed and when it is owed and how it is paid. The second document is a Land Trust Deed or Trust Deed depending on where the property is located.

The Land Deed of Trust transfers ownership of the property from the seller to a trustee, usually the attorney who prepares the document. This document explains all of the terms and conditions of the deal including default, legal fees etc. The trustee is a third party holding the note for the benefit of both parties.

Should the buyer fail to pay, the trustee can foreclose and the lender can sell the property.

An example of a Land Deed of Trust is below from Fannie-Mae. This one is for the state of Virginia. The form is similar from state to state. Laws vary from state to state so this is just an example, your closing attorney will of course have the correct form for your state.

Seller Default

Seller defaults can be problematic for a wraparound note. As mentioned above, there is no reason for a seller to default as long as the buyer is making the payment. During the process, the seller will be required to produce a mortgage statement for the buyer from the most current month verifying that the payments have been made on time.

Part of the agreement will include a provision that neither party will be permitted to borrow against the property. During the agreement term, the loan must remain in place as is. It seems strange that the buyer will be making a payment that is greater than the required payment but that’s not the case.

Remember this is a sale and not a rental. The buyer must be told at the time of signing the agreement that they are 100% responsible for all maintenance on the property. This can include installing a new AC unit or making any major repairs, it is their house. As a seller, you will not loan any funds to make repairs.

The promissory note will include a provision for the seller to inspect the property. It is important during the period of the contract that the seller inspects the property because at this point the seller is the Mortgagee or lender. You as a seller have stepped into the role of the lender.

Buyer Default

What happens if the wrap borrower defaults? The Mortgagee or lender will know immediately when the payment is not credited on time. Most traditional mortgage payments are due on the first day of each month. The payment on the wrap-around loan should also be on the first day of the month.

If the buyer does not pay on time, you have about 12-14 days to make the payment in their place from the funds you put aside at closing. You can start the foreclosure process after the first payment is 30 days late. Check the laws where the property is located. A demand is issued for the remaining balance on the loan and if they fail to pay, you can repossess the property and resell the property.

You may be fortunate and find that the property value has increased in the two years since you sold the property. You could also rent the property or refinance it. If the seller paid the monthly mortgage on time for a few years you should be ahead financially.

Bank some of your income for a rainy day

If you as the seller have been conservative with the entire transaction, you have been banking some of the funds paid directly to you each month by the buyer. In the example above that amounts to over one thousand dollars each month. Perhaps you put aside half of it or the entire amount for a rainy day. If you have a good reserve, a buyer’s default should not be a financial hardship.

Your decision as a seller to replace a traditional mortgage lender means you have set up the financial decision-making process. Many articles explain what a wraparound mortgage is hopefully this article has explained to you as a seller and to real estate agents how the process is implemented.

Why the sales price can be higher and why competitive rates are not applicable in this situation? An appraisal is not necessary in this transaction on the seller’s part because the seller sets the price. The buyer’s loan is based on the agreed price without regard to an appraisal.

Don’t over price, buyers need to refinance

Sellers will want to offer their property at an amount that it would appraise for. Remember the buyer must finance the property at the end of the balloon period. It may seem that most of the terms are in favor of the seller and they usually are even in traditional lending.

The seller to protect the asset should be prepared to stay in communication with the buyer by reminding the buyer how many months are remaining on the mortgage and encouraging them to follow some simple guidelines six months out from making an application.

This can include not opening any new credit accounts, not buying a car on credit, and being prepared to have the required down payment if the equity in the house is not sufficient. Their mortgage balance will not have been reduced very much during the few years of their loan.

Checklist for Home Sellers Offering a Wrap-Around Mortgage

1. Consult with a Real Estate Agent:

- Contract: Establish a clear contract outlining the agent’s duties, commission, and responsibilities.

- Commission: Determine the commission you will pay to your listing agent.

- Buyer’s Agent Commission: Decide if you will pay a commission to the buyer’s agent.

- Marketing Strategy: Discuss effective marketing strategies to attract potential buyers.

2. Determine Property Details:

- Selling Price: Set a competitive selling price based on market analysis. Your agent can provide this

- Interest Rate: Determine the interest rate you will charge the buyer, considering factors like market rates and your desired return.

- Balloon Payment: Specify the term for the balloon payment, which is the lump sum due at the end of the loan term.

- Down Payment: Determine the required down payment amount or percentage of the selling price.

3. Calculate Monthly Payments:

- Principal and Interest: Calculate the monthly principal and interest payments based on the selling price, interest rate, and loan term.

- Homeowners Insurance: Estimate the monthly cost of homeowners insurance.

- Property Taxes: Determine the annual property taxes and divide by 12 to get the monthly amount.

- HOA Fees: If applicable, include the monthly HOA fees.

- Total Monthly Payment: Add the principal, interest, insurance, taxes, and HOA fees to determine the total monthly payment.

4. Legal Considerations:

- Closing Attorney: Locate a closing attorney specializing in real estate transactions.

- Loan Documents: Discuss the necessary loan documents with the attorney, including the promissory note, deed of trust, and any additional agreements.

- First Mortgage Call: Address what will happen if the first mortgage holder calls the loan.

- Late Payment Fees: Determine appropriate late payment fees.

- Foreclosure Costs: Discuss potential foreclosure costs if the buyer defaults.

- Early Payoff: Specify if there will be any fees for early payoff of the loan.

- Property Liens: Ensure that neither party can obtain a loan against the property.

By following this checklist, you can ensure that your wrap-around mortgage arrangement is structured legally and financially sound.

Summary

Offer to finance using a wrap-around mortgage when you need to sell your property fast at a realistic price. As a seller, you will receive cash for your property at closing. If you do not have a place to park that cash, earning 9% interest even for a few years may be a good option.

Work with a good real estate agent familiar with wraparound mortgages and a closing attorney who can prepare the documents. After closing, continue to communicate with buyers who are now the Morgators.

It will be important for a real estate attorney to craft a document incorporating the elements listed here that are appropriate to the loan and state law. In the Eastern and Southern United States, closings are typically done at an attorney’s office. The seller should consider using a closing attorney to craft the documents including the trust deed and note.

This article does not intend to provide legal advice about wraparound mortgages nor does it confirm that the elements listed can be legally implemented in all jurisdictions. We are not responsible for your use of anything listed in this document. As a home seller, you should seek professional advice not only from a real estate attorney but your CPA regarding tax issues.

We are here to help

Logan-Anderson Gulf Coastal Realtors has experience working with clients who have offered wrap-around mortgages to buyers. We have also worked with buyers who have taken advantage of a wraparound mortgage. Contact us if we can help you.

More articles will be created that dive into some of the terms discussed here. Please check back or better yet, subscribe to our blog.

![Why is the short-term rental market underperforming now [2025]?](https://gulfcoastalrealtors.com/wp-content/uploads/2023/06/vacation-rental-.jpeg)