Last updated on July 24th, 2022 at 07:55 pm

Last Updated on July 24, 2022 by

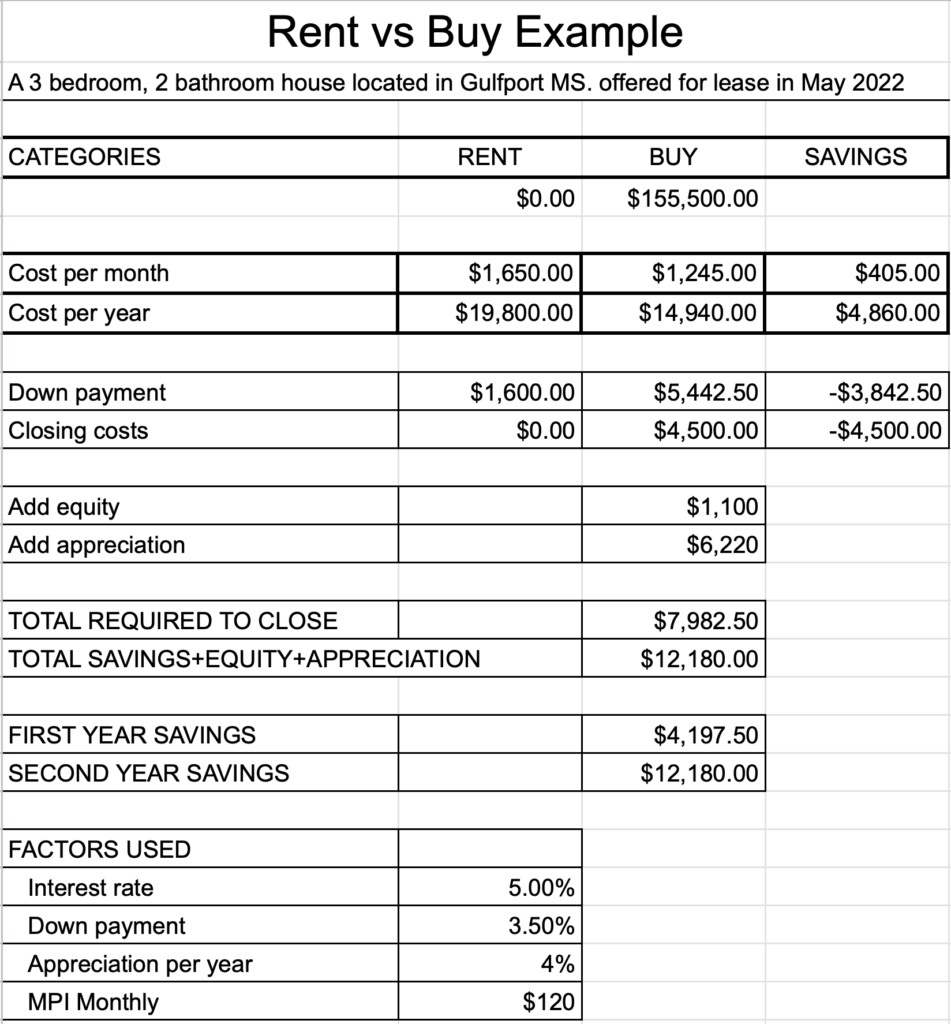

Why are you renting when you can buy with as little as a 3.5% down payment and a good credit score. Your rent is $1,650 and the mortgage payment is $1,245 per month. This is an example of real rental property and what it would cost to buy that same property? You should buy Vs. rent a home: now.

Higher home prices and higher interest rates will change the numbers presented but rents are going up as well so I believe the numbers are relative.

I just received a notice today about a house that has been offered for rent at a rate of $1,650 per month. This home’s value is about $155,500. Read on to see how it was cheaper to buy vs rent this same home.

The lease payment is $1,650, your mortgage payment is only $1,245

The required lease/rent payment is $1,650 per month. You can see that the estimated monthly payment is $1,245 per month saving you $355 per month. Interest rates are going up so we used a higher rate in our calculations.

If you bought this house, you would save about $4,260 per year at today’s interest rate vs paying rent. Rents will continue to increase while the principal and interest on a fixed rate home loan will not. To be fair, insurance and mortgage taxes can increase and probably will.

The dollar amount of those increases may be competitive with the dollar amount of your rental increase. Year after year. The evidence is adding up, you should buy vs. rent a home: now.

Your $1,600 security deposit can be applied to the downpayment

When you rent this house as your primary residence, you will be required to make a security deposit of $1,600. The required down payment based upon the purchase price of the house ($155,000) would be $5,442.50 (3.5%).

To make a direct comparison, you would deduct the $1,600 security deposit against the closing costs Paying the security deposit is somewhat similar to making a down payment this is why both are compared. To make the example simple, we deducted the deposit from the down payment and show that you will owe $3,842.50 more than the security deposit to make the purchase. In other words, you are about 1/3rd there already.

Look at that equity

The time to add equity is the amount you pay each month which reduces the mortgage balance. The equity paid in is about $1,100 for the first year. This amount goes up every year just as the amount of interest in the monthly payment goes down. This is in effect, a savings account.

You may not live in the house for 30 years to pay off the mortgage but every year you stay, the debt is reduced which means over time, you have built up some value. You should get back all of this value when you sell the property. Assuming of course that the property continues to appreciate.

A look at appreciation

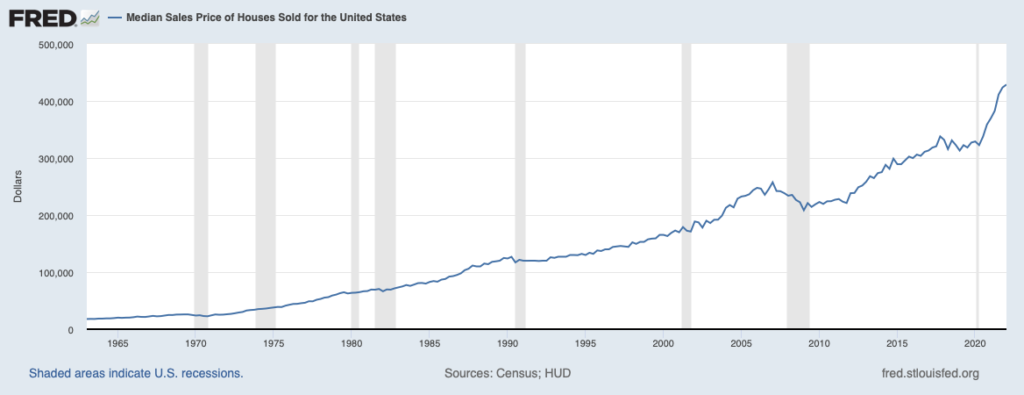

Now, include the estimated appreciation of about $6,220 per year. This is a big one. The chart above from FRED shows clearly that while there are dips in housing prices, they always recover. If you stay in your home for five years, you may have accumulated a total of $31,100 in appreciation at 4% per year (below the current level).

Add to the appreciation of $31,100, five years of equity at $1,100 per year ($13,200) for an increase in your net worth of about $44,300. I forgot to mention that the $44,300 is not available if you rent for the next five years. Are you motivated yet?

Funds to close

The total money you will provide at closing is about $7,982.50 which includes the down payment and closing costs. Closing costs include insurance for the next 12 months, a reserve for property taxes (due at the end of the year), and a reserve for insurance. The new mortgage will require these reserve funds. In addition to the taxes and insurance will be a one-time fee for your mortgage insurance premium.

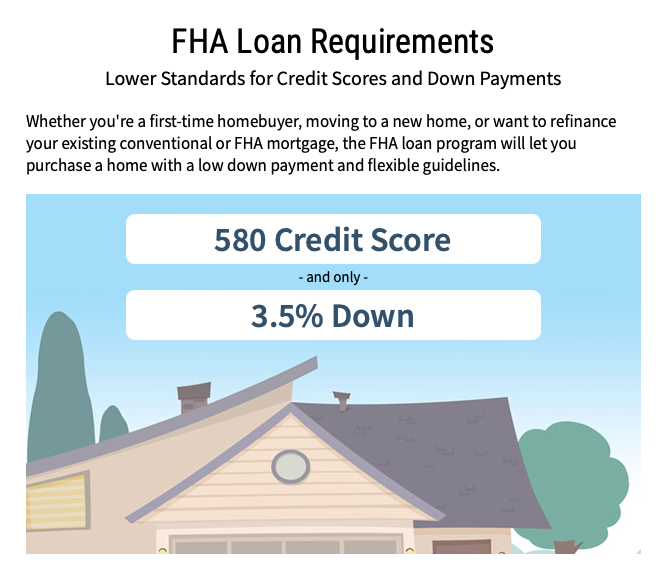

When you receive an FHA loan, you are charged a fixed fee upfront in closing for a “mortgage insurance premium”. In addition, an amount is added to each monthly payment for the monthly MIP. You owe these fees because you only put down 3.5%. If you would have put down 5-19% on a conventional loan you would have paid private mortgage insurance or PMI.

With 20% down there is no added insurance. This insurance premium is a way to protect the government from defaults. The theory is that a lower down payment means less “less skin in the game” as some say. If you have little to lose, you may walk on your mortgage debt.

The big payoff

Now see how these closing funds will come back to you. In the first year, you will save $4,260.00 buying vs renting. Add to this the equity of $1,100 and the appreciation of $6,220 and your total savings over renting for the first year equal $3,597 (after deducting downpayment and closing costs).

This is after deducting the down payment and closing costs. Of course, you will not be able to bank all of your savings. Remember part of the savings is in equity which is available when you sell the property. The same with appreciation. Regardless, the numbers are real even if you have to wait until you sell to get the funds back.

The big payoff is that you will save $11,580 every year based upon the factors used vs renting. The actual cash savings will start at $4,260 or $355.00 per month you save immediately when exchanging rent for a mortgage.

Your starter home will become an even better decision as you see the value of your home increase over time. You should buy vs. rent a home: now, a reoccurring theme as I explain the savings over and over again.

About that rent

Remember that rental payment of $1,600? That owner had recently raised the rent from $1,300 to $1,600. Do you think that the rent will continue to increase over time? Let’s consider this for a minute. Starting at $1,600 per year assuming that the property owner will raise your rent by 4% per year. In five years your rent will be hovering around $1,900 per month.

To make a fair comparison, your principal and interest payment will not increase (a fixed loan for 30 years). Assume that insurance goes up 4% per year. I estimate that to be about $100 per year. Taxes may go up 4% as well as another $100 per year. A total of $1,000 more in five years. An increase of $84 per month.

Compare the $84 increase to the $300 increase in rent each month. Do you think renting is better than buying? Which is the smart move. Renting or buying?

Do you have the closing funds?

One of the most essential factors in the decision-making process is to determine if you have the funds for the down payment and closing costs. The good news is that with this program you are permitted to receive a gift of the funds or borrow from your 401k. These may be good options if you are short of what is required.

You are not permitted to incur debt to borrow the down payment or closing costs e.g a lending company. Lots of first-time homebuyers receive “gifts” from their parents and friends. These gifts are not intended to be repaid which is why they are permitted.

In real life, people ask their parents for money for a down payment and eventually give it back to them even though there is no contract or official requirement to do so.

Monthly savings can help repay a 401k loan

When the monthly savings is so large as it is in this scenario between buying vs renting, you could decide to return the funds with the savings. Even if you were gifted the entire amount (about $10,000), you could return this amount in about 3 years ($300 per month at 5% interest will pay off $10,000 in three years).

[First-time home buyers, read this about your budget]

You can borrow from your 401k, that is permitted. The scenario above is the same, you can repay that 401k loan with your monthly savings. You are generally permitted to borrow up to $50,000 for up to five years from most 401k programs.

Watching your home’s value go up

Watching your home’s value go up year after year is like watching a savings account grow. With this house and this monthly rent, buying makes the best financial sense. Putting that extra money in your pocket every month and owning your own home is far better than making monthly rent payments.

What the landlord did with this house

Housing prices have increased since this property was sold in 2020 for $130,000. The buyer thought this to be a great investment at that time, to provide rental income. Just after the property was purchased it was rented. The rent started at $1,300 the first year and then went to $1,600 the next year.

The investor is into the property for the long term. They know that people will rent rather than buy for a variety of reasons. I believe one reason is that some think they will not qualify to buy or that they can not afford to buy.

Rental properties can be the better choice when the rent is lower than the mortgage and other costs to buy. The smart financial move is to buy when the numbers work. Not every area can boast that their homes are more affordable than renting.

You should buy vs. rent a home: now

The landlord understands that you should buy vs. rent a home: now, they are just providing a service and earning what may be a good income in the process. I often work with investors to do exactly this. At the same time, we work with people like you who can qualify to buy.

Let those who can’t qualify to buy rent, you should be buying. The title of this article You should buy Vs. rent a home: now. is true. Now is the operative term. Every month that goes by costs you about $400 plus equity and appreciation.

Government loan programs help

The tiebreaker is the FHA loan program which allows people to participate in the American dream. Unfortunately, many first-time would-be buyers are not aware of these programs. There are other programs as well including the FDA program which permits a purchase without a down payment.

Your first home can be within your reach with a little investigation. I strongly advise anyone who is renting to contact a realtor and ask them if it is possible to buy for what they are paying in rent. It may be the right time for you. There are significant financial benefits to buying vs renting as we have explained above.

It would not be fair to leave out other monthly costs of owning a house. These costs include landscaping and maintenance you are not required to do at a rental property. Maintenance costs are always part of homeownership. Making home improvements is part of the fun of ownership.

There are more benefits above the monthly savings?

Now for the benefits which include tax advantages, additional living space, an increase in the home’s value, and more. I have held back on discussing these other benefits because frankly, with all of the financial benefits above, who need more reasons to buy?

Tax benefits are not as great as they once were. The current standard deduction overcomes the need to have a mortgage deduction for many. If the tax regulations change this could come back. For those with large deductions, the house interest rate and taxes may help reduce your overall tax due.

It’s yours. This is a good reason by itself. Paint the rooms any color you want. Some say that buying a home should not be considered a good investment. I disagree. The vast majority of wealth in this country comes from equity in private homes.

This house is but one example of buy vs rent

This house is only one example of a property that rents for more than the total monthly cost to own it. It may be difficult to find a house in your area where you can buy better than rent. These properties are out there. Why not let your real estate agent do the work for you.

The first step to take is to contact a real estate agent in your market. Then contact a mortgage lender to determine how much house you can afford. Tell them you are a first-time home buyer if that is the case. Since you are buying your new home, you want to explore mortgage rates and the overall housing market.

There are some areas where you can not find a selection of homes that are less costly to own than to rent. I know of an area where it’s fairly common. The Mississippi Gulf Coast. People working manual labor jobs, restaurant workers who own their own homes. Our cost of living is far lower than in California for example.

The example above is located in Gulfport, Mississippi

The example above is located in the city of Gulfport, MS. Other properties are less costly to buy than paying rent in this area. I picked this one because it popped up and gave me the idea to write this article.

Read this article about the best places to live on the Gulf Coast.

If you can afford a 20% down payment, the houses are even more affordable without mortgage insurance. The more you put down, the lower the payment. I also suggest that you consider putting down only as much as necessary to make the payment comfortable.

Over the years, your property will work for you repaying you for buying it. As mentioned above the appreciation and build-up of equity are great benefits.

Time to get pre-qualified

If you see what we see in this article, it’s probably time to get pre-qualified. See how much home you can afford. Read our article on this site “Serious about buying a home? Get pre-qualified or lose out.”

While it’s still a seller’s market, you need to know that you can buy a home before you can make an offer. When you decide you want that house, as the article will say, move fast with that pre-qualification letter. Read this article “can I qualify to buy a house?”

Click here for a form to get started on your pre-qualification.

Millennials (and others) read our series of articles about Financial Resources for Millennials. Starting with this article which is a directory of the series. The series is directly related to the content of this article with lots of tools to help you understand home buying.

Contact us, we can help you find your affordable home

At Logan & Anderson, Gulf Coastal Realtors, we are at your service. Our specialty is helping first-time buyers locate that perfect home, they can afford. We help people relocate to the Mississippi Gulf Coast as well.

Our blog site LoganAndersonLLc.com has lots of articles about things we have discussed above. You can also check out an article about Mississippi Gulf Coast Housing. To learn about qualifying for a mortgage click here.

PODCAST BELOW