Last updated on November 4th, 2022 at 09:41 pm

Last Updated on November 4, 2022 by

Let’s get started. I am assuming that you are ready now to find that house, correct? You have read the other articles in our Millennial Financial Resources Series so we need not go over all of that financial stuff now. On to the best part of the entire process, getting to that property. There is one important first stop for the first-time home buyer and that’s looking for and selecting a good real estate agent. The home buying process requires many steps and our real estate agent will act as your guide.

The best way to look for a good agent is to ask friends and relatives who have worked with agents in the same area. As I am writing this, it’s still a seller’s market out there so you need an agent more now than when it’s a buyer’s market.

Just checking before we wade into this topic, you do have a pre-approval letter? If not, you have missed many steps in the process before selecting a real estate agent. Now would be a good time to backtrack and read our series of articles listed at the bottom of this article.

Ok, you said yes, you forgot that you were pre-approved by Ajax Mortgage company and ready to go. Back to the real estate agent. Now that you have worked down your list of agents recommended by your friends, it’s time to meet with the agents and their brokers. It’s a good idea to meet with a broker as well as the agent to be sure you are selecting the right agent for the job.

Real Estate Agents work for sellers at NO COST

Tip: Real Estate Agents working for buyers are usually compensated by the seller’s real estate broker from the proceeds of the sale. Your agent works for you at NO COST. Don’t even think of going to an open house or looking at a home for sale without being represented.

As a real estate broker, I love it when the buyer and seller are our clients but that is not always best for the client. The real estate agent has a fiduciary responsibility to your client. A real estate agent representing the buyer owes loyalty first to the seller. It’s a dilemma in our industry and there is a process to work it out when it happens. Usually, the broker will ask you to work with another agent at the brokerage not involved in the transaction.

The Real Estate Agent Interview

This is an interview, you must feel comfortable with the agent or ask the broker to recommend another agent. If the entire situation seems odd, try another agent at another brokerage.

Be clear about what you are looking for. You should give the prospective agent a list of your wants and your needs. There is a difference. You may want a four-bedroom house but you need a three-bedroom. You can’t get by without at least three bedrooms but that fourth would be great. Check out this list:

- Price range from $250,000 to $300,000. Want to keep at $250,000 higher would be meeting wants

- Need at least 3 bedrooms – Want 4 bedrooms

- Need at least 2 bathrooms – Would like 2.5 bedrooms or even 3 bedrooms

- Need 1,800 square feet – Would like about 2,200 square feet

- Need two car garage – Want three car garage

- Need a fenced yard – Want a fully landscaped yard

- Need a single-story house – In this case, a two-story will not work because of health issues

- Need a cul-de-sac house for the safety of children – Would accept a house on a non-busy street

- Need privacy, seclusion no city living – Would accept a development house on the fringes with a view

- Need two sinks in the master bathroom – Would accept one sink with a large counter

- Need area with schools that have very high ratings e.g. 8-10 – Would accept 7 if good local reviews

- The area does not permit on-street parking, homeowners association fees are ok

- The swimming pool is a positive but not a need. If no pool, we want to build one

- Interested in the Serenity area would look at homes in a like area

- Need a 30-day escrow, we sold our house and are ready to move at closing.

- A home inspector is required and we are willing to pay for an inspection.

You have selected a real estate agent and now it’s time for the home search. But wait, the paperwork starts now. Your agent just pulled out a document they want you to sign. “Working with a broker”. The agent should explain that the form is required by the State Board of Real Estate. This form does not contact but it does inform you that you are working with a licensed broker or their licensed agent. Fear not, it is just a disclaimer. Read it and sign it. You are not married to your agent. Incidentally, it’s time to explain how agents and brokers work.

A broker has a license issued by the state. A broker who meets qualifications may sign licensed real estate agents to work under their license. All sales are made by the broker even though the real estate agent seems to be doing all of the work. Real Estate agents are self-employed, they do not work for the broker.

Real Estate Agents must work under a Real Estate Brokers License

All commissions from sales go to the broker and the broker will compensate the agent. Buyers and sellers can never offer any form of payment to a real estate agent. All funds must to the broker.

You will notice that all legal forms related to real estate transactions have the word broker on them. Your agent is representing the broker and has the broker’s permission to sign real estate transaction forms. Starting with working with a broker, there will be more forms to come.

Lots of people look at homes on the internet and you should as well. Ask your agent to sign you up on their website so you can flag homes that look good to you. At the same time you are looking, the agent is looking. Your paths will cross many times during the search. At this point, the first step is to make a list of the homes you want to see. As potential buyers with a mortgage pre-approval, your agent should have no problem getting appointments for you.

Market conditions are changing as I write this. The current market could go from a seller’s market to neutral during your search which is good for you. There is a good chance that the seller may be willing to flex on the price or closing costs. Do not be in a hurry to buy a house even if you are living in a hotel. There is a right time for rushing and buying your first home is not that time. It’s in your best interests to carefully look at each house and compare.

Take your time deciding on the right home then run fast to the offer

Your agent will not decide for you but a question that I like to ask is “If you were me, would you buy this house?”. If the agent says no, ask why. It may be that your agent spotted something that they are concerned about. Now that I just said take your time, I will suggest that you make a quick decision. This is what I mean. After you have seen several houses in person and on the internet, you should have a good idea of what you want.

up close when you have selected a few houses you are interested in it’s time to see the up close. At the rate homes are selling, if you have fallen in love with a house, you should put in an offer as soon as you have made up your mind.

Wow, this sounds like a word salad. True. Take your time when you start looking around. Get a feel for the types of houses that you like best. If you were buying on the Mississippi Gulf Coast, you would see a wide variety of house types such as:

- Craftsman early 1900’s houses, small e.g. 1,100 sq ft, three bedroom one or two baths.

- Mid-century homes were built from the 1950s through 1990. These are usually found in developments and are a little larger e.g. 1,600 sq ft or more. Some have a garage. 3-4 bedrooms, 2 bathrooms.

- Early 2000 were located as custom homes or in developments. Usually larger homes over $2,000 sq ft, 3-5 bedrooms with 3 or more bathrooms

- New builds are available now or to order. Various sizes mostly in planned developments with HOAs. Larger homes are similar to the early 2,000s. with garages

- Beach custom builds. Buy the land and design a home near the beach. Insurance requirements often require beach close homes to be elevated.

I am sure that I have left out a few types but these are the basics. There are many homes in all of the categories to choose from. Almost anyone can live in new build-in development but living in a house built in 1880 or 1910 is for a selected few. Some people love to live in an old remodeled house. Be sure your real estate agent takes you around to the various styles of homes so you can drill down to the style you want to look at. When you have decided on the style of home, there are usually enough of your selected style to visit.

The bidding wars

Recently some houses were subject to a bidding war. This type of situation is fading away as the market is cooling down. Only go to an open house if it’s one on your list. Remember, your agent can get you into any house for sale by making an appointment.

At this point, you may have found what you believe is the ideal house. I strongly suggest that you return a second time before you write the offer. Take a pad of paper and your phone camera. Make a list of things that you do not like. Items that require fixing. Take lots of photos and a video of the house. This is your pre-inspection tour. Discuss our findings with your agent and come up with a list of things you want the seller to do. A word of warning. This is still a seller’s market so tread lightly with your requests.

The seller is required to complete a PCDS (see above example) for prospective buyers. You are required to sign that you received a copy of this document which your real estate agent will provide to you. This is the starting point for a good look at the property. The owners must disclose important information to you about damages in the past and repairs. A good example is a house that sustained a bad fire five years ago and was repaired.

You and your home inspector can look for anything they may have missed or the quality of the repair. There are some important things listed in the PCDS that can help you later such as the age of some items e.g. water heater.

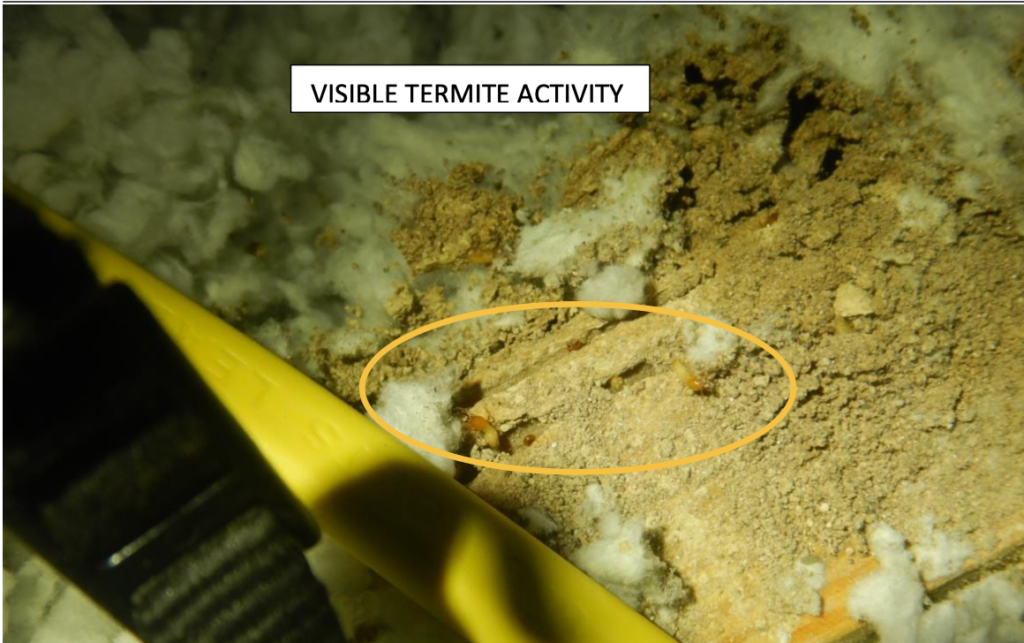

I found termite repairs listed on the PCDS

Some houses have been flooded and if so, they must state that and what repairs were done. The best time to decide if you want to buy this house is after reviewing the PCDS. I looked at one PCDS and discovered that there were extensive termite repairs. A friend with lots of construction experience went to the property with me and looked around. He found active termites. Given the previous damage and the active termites, my client decided not to make an offer.

The PCDS can not always be relied upon to provide any good data. If the seller bought the property to flip it and did not live in it, they are not required to check any boxes where the question relies on personal experience of which they have none. In my experience, few potential sales have fallen through because of the PCDS. There may be some valuable information on the PCDS such as the age of the room.

Tip: Always have your agent ask the buyer when the roof was replaced. An exact date and information about the roofing company are very valuable for insurance purposes.

You want those missing shingles replaced

When you have narrowed the list to a few major issues if there are any, the agent will address them in the offer. For example, last year a storm blew off a few shingles. You want those replaced. The carpet in the living room is terrible, you want that replaced. Your list was growing but the agent told you there is another time to deal with that as part of the home inspection.

FHA loans will require some repairs of safety and health items before they will fund a loan. The same is true of VA loans. If you are applying for a VA or FHA loan, ask your agent if she/he thinks the house would pass their inspection.

You may have selected the best house but the agent may tell you that it may be unlikely that FHA or VA would approve of the property. At this point, it would be time to move on. You can’t fight FHA and VA.

Assuming that this discussion is rhetorical and your small list of items is not a deal killer, your agent will include a statement that the seller repairs the items before closing or that they reduce the selling price by the cost of repairs, It’s time to determine what you will pay for the house. You will arrive at the purchase price offer.

Sellers are asking$300k, the estimated value is $305,000

For example purposes, the house is listed at $300,000 and your agent has done some work to determine it’s worth about $305,000 which means the asking price is good. You are asking the seller to spend $2,000 on repairs.

Considering these numbers and the current state of the real estate market, you decide with your agent’s help to offer $295,000. This is $10,000 under the estimated value and the seller will pay $2,000 in repairs. Do you think this looks fair? You would like to offer $280,000 but your agent recommends against that because there are still more buyers than sellers out there and the seller could wait for a better offer and not wait long.

Tip: Real Estate agents perform a survey of pricing in the area of the home you have selected. They create “comps” which are valuable in determining a fair price to ask. They also keep up to date on market trends such as prices moving up or down, days on the market, etc. All of this goes into their recommendation to you. In the end, you are in charge and your real estate agent will offer the price you decide upon.

Your real estate agent provides input, you make the decision

The offering price should be consistant with the market and consider trends. What if the seller does not accept now? Will they get more or less later.

Ok, you agree to this offer of $295,000 and offer a $500 earnest money deposit. At this point, you should know what an earnest money deposit is. These are cash fund that is being held in escrow by the broker or escrow officer until the contract is executed. At that point, the earnest money is applied to your closing costs and down payment. You can lose the earnest money if you fail to perform which means you back out of the deal. You can terminate the deal if any of the contingencies are not met.

The seller rejects your offer, what now

What happens if the seller rejects your offer? They must reject it in writing at which point there is no contract. The seller may decide to “counter offer”. You offered $295,000 and asked them to pay $2,000 for repairs. Their counter offer is that they want $300,000 and they will pay $2,000 in repairs. You discuss this with your agent who tells you the house has an estimated market value of $305,000 so accepting their counter would be a good move.

If you agree, your real estate agent will prepare the counteroffer and have you sign it and submit it back to the seller’s agent. Assuming they agree, you have a valid contract.

Another scenario is that you decide to counter their counter. Yes, this is a thing. You may want to split the difference between their $300,000 and your original offer. Your agent tells you that the best move here is to ask for $2,500 in closing cost assistance and keep the selling price at their counter price of $300,000.

You agree this is a good offer and your real estate agent will submit the counter to the counter. If the seller agrees, you have a valid contract and can move on to the inspection.

Time to discuss the standard contract for the sale and purchase of the real estate. The sample above when filled in and signed by both parties forms a legal contract. Performance is required by both parties. You the buyer must have the funds to close and take possession on the closing date (unless a box is checked with another date).

If the contract is signed, can the seller accept a better offer?

The seller must deliver the property in the same condition as you have viewed it just before closing. A breach of either side will come with consequences. The seller for example can not just back out and tell you they found a buyer who will pay more. You can’t just say you had a bad night before you signed the contract and want to back out.

There must be valid reasons for terminating the agreement and those are listed in the agreement. As a buyer, if your financing falls through, you are permitted to back out. If the buyer admits to errors on the disclosure form, you can back out. The point here is that there are “contingencies” that permit the parties under those circumstances to terminate the agreement. Under special circumstances, you can therefore receive your earnest money back.

You have a valid contract at this point which starts the clock ticking on the closing date which is in the contract. The closing attorneys or escrow company will be notified by one or both real estate agents when they receive a copy of your agreement and the signed PCDS. You may also be required to sign a lead paint disclosure depending upon the age of your property.

How much will I need at closing

Closing costs, what are they? KEYLADDER has identified more than 27 items that are on the closing disclosure many of which require fees or deposits in addition to your down payment. It’s important in the early stages that you identify the closing funds you will need in addition to your down payment. One way to determine what these costs are even before you sign to buy a house is to use the unique calculator embedded in this unique article from KEYLADDER titled “The best free mortgage costs calculator: get it here”.

This article goes into debt about closing costs explaining each of them and why they are on the disclosure. You should understand what you are paying for in advance. This article can inform you.

Do I need a home inspection?

It’s the time at this point to order your home inspection if you choose to have one. You will have to pay this cost either on a credit card or check or it will be added to the closing package and paid at closing.

There is a provision in the contract for a home inspection. Assuming you checked it, you provided a specific number of days to get this done. You should follow up to make sure the inspector gets to the house on time and the report comes back on time. The contract specifies that you have x days to review the inspection and respond to the sellers with any requests or simply to say the contingency of the home inspection is completed.

Because you have done your inspection as discussed above and have reviewed the PCDS you are somewhat knowledgeable about needed repairs. The home inspection may find hidden things that you were not aware of. Go through the report with your real estate agent. If the estimated cost of repairs is within what you have already asked for then this task is done. If the inspector finds something major such as a missing downspout causing erosion, you may want to ask for this to be fixed. Perhaps a roof ridge cap is missing, add this to the list.

Can the seller refuse to fix problems found in the home inspection?

Your real estate agent will tell you that the seller is under no obligation to fix anything on the list. If you bring a long list of small stuff and/or make the list problematic for the seller they may back out of the deal. I backed out of a deal to sell one of my houses because the buyer wanted about 20 nonsense things fixed.

One of the problems is that the fixes had to take place before closing and I could not have found contractors to do the work in time. My real estate agent sent a contract addendum over terminating the contract because of maintenance issues found during the inspection.

Assuming that you work out something with the sellers and they agree to fix most or all of the items on your list, a contract addendum will seal the deal. The next hurdle to get over is the “Wood Destroying Insect Report”. I call it the termite report. The seller orders and pays for this report. It takes about a week or two to get this report. The seller’s agent must order the report as soon as you have settled the home repair items.

What if there are no WDI’s?

You may wonder why the home inspector does not list termites or other WDIRs on their report. That’s because it takes a special license to generate a report listing termites and other pests. The building inspector may point out termite damage but not any active infestation. Assuming your dream house has no termites, the report goes into the closing file. If there are active termites, the seller will expect the termite company to perform repairs.

The lender may not permit you to close if there are active termites so remediation must be done immediately. Many discoveries of active termites can be corrected in a week or two with chemicals, traps, etc. A problem that may be more serious is if there is actual structural damage that can cause issues in the long run. Remember that clock? There are so many business days left to meet the closing deadline so all of these activities must move forward as fast as possible. This is where real estate agents earn their commission.

You and your real estate agent can’t take your eyes off the ball until you are sitting at the closing table or offered the closing documents to sign. During this process from signing to the closing, you may want to visit the property again for measurements. Often an agent is asked to let contractors into the property to measure for carpet etc. Your financial institution should be in regular contact with you and your real estate agent about their progress with your loan.

Always one more thing to get done

And yet another thing to get done. You will need to buy a homeowners insurance policy for your home. The cost of that policy will become part of your monthly mortgage payment. I am not going into the process of buying insurance because we wrote an entire article as part of this series on Millennial Financial Resources.

Please read this article so that you understand this important aspect of buying your house. Your home purchase is not complete without adequate insurance coverage to protect you and your lender.

Give your insurance agent all of the details about closing including the name and contact information for the escrow/closing attorneys. Your real estate agent will send over to the closers their invoice for the policy along with information that the lender requests to verify coverage. Tip: your credit was checked at the time you applied for the loan. The insurance agent will check it again before issuing the insurance policy. Be sure you don’t incur any more debt before closing.

In the background, the closing attorney or escrow office must secure a title insurance policy for the property you are buying. This policy is issued after a detailed investigation of the property title history to make sure the seller owns it and can sell it. Sometimes issues develop where the title is not “clean”. Perhaps during the previous sale to the (now) seller, a deed of reconveyance was not created making the seller, not the owner. This is the type of thing that the title insurance company can work out. After the issue is fixed, they order a title insurance policy.

What’s happening in the background and what is that appraisal all about?

Your real estate agent estimated the sales price of your target property to help you make an offer. A professional selected by your financial institution selects a licensed appraiser to look at the property and evaluate the actual value. You are prepared to pay the contracted amount of $300,000 but what if the appraiser determines it’s worth $295,000?

In this case, you have options:

A. terminate the contract because the lender will not approve a loan for more than the appraised amount (there is more to this but good for now).

B. Ask the seller to lower their price to $295,000

C. You come up with the shortage of $5,000 as a larger downpayment

D. Split the difference between buyer and seller

Any of those choices will make this happen. You could split the difference with the seller. My client was in a similar situation. There was a $10,000 gap. Each agreed to cover $5,000. The seller lowered the selling price by $5,000 and my client came up with an additional $5,000. The deal was back in balance and it went to closing.

The CD can not be issued until the appraisal comes in and is cleared. You may ask, what happens if the appraisal is higher? Nothing. You will just feel better that you got a deal and the seller will feel worse for leaving money on the table.

By the way, you pay for the appraisal in your closing costs.

What is the next step?

Recently, a client was buying a house. The owner’s closing company failed to complete the title transfer from the previous owner. It took four days to track down the person who could get the problem fixed. This almost delayed closing, it was the last thing needed to issue the CD.

The next step in the process is the closing disclosure which the lender will send to you and the closing office. This occurs three business days before the scheduled closing date. The CD lists all of the costs to acquire the house including the mortgage interest rates which should match what you were quoted. At this point, your lender will pull a credit report to verify that you have been good and have not caused any wrinkles in the system by signing a contract for a new car.

Now that you are three days away from closing, it’s time to wire the closing funds to the closing attorney. Obtain a copy of the final closing cost estimate from the closer. Send exactly what is requested on the closing estimate. This amount may be more or less than you were prepared for because some costs change with time e.g. daily interest. Make sure that the closing funds will arrive at least the day before closing before 3:00. If you live on the West coast, consider the time difference. The funds must be in the closer’s account before closing. Two days before closing or sooner is best.

When can I close? Does anything else need to be done?

Now for the closing. You may just sign documents and send them overnight or you can appear at the closing table.

Time for Murphy’s Law to come into play. You lost your job a week before closing. During the last-minute check before the CD is issued, the lender calls your employer (former) and finds you no longer have a job. Ouch, the deal is dead. Let me explain what happened when my wife and I arrived to close on our current house. We drove from California to the Mississippi Gulf Coast.

The closing was scheduled for noon. We arrived on time and started to review documents. We had not seen the final closing documents which were prepared after the CD was issued. The closing cost estimate was adjusted after the first one they sent.

I looked at the amount to close and noticed that it was short by about $10,000. Funds had already been wired the funds and now I was in a state where my bank did not have a branch. I asked if I could borrow their computer and looked at my account online. There feature that permitted me to send a wire. After entering the amount and pushing the button, I asked the closer to call their bank. The funds were in their account in a few seconds. Fortunately, I had sufficient funds available but what If I did not?

When can I get the keys?

There are circumstances where you can not get the keys at closing. If it’s too late in the day to send wires from the lender to the closer or the closer to the mortgagee. This is called a “dry” close where all documents were signed but funds were not exchanged.

Technically there is a sale and property transfer but contract law requires consideration and without funds, there is no consideration. This could happen on a Friday late in the day or around a holiday.

It’s time to say thanks to your loan officer and real estate agent. You now have a new home with a home loan. You have joined other first-time home buyers in the American Dream. But wait! Now it’s time t move in and decorate and make the property your own. Who is going to pull weeds and cut the lawn? Please read our next in-the-series article titled “What Comes After Buying the Dream House”. If you have not read our other articles listed below please do so.

I hope that this article is helpful to you. This is one of a series of articles written specifically to assist Millennials to succeed in life. Many parents of Millennials did not have the skills to teach their children some of these life skills. Hopefully, this series of articles will help you. To get the most of them, please click on the other articles in the series that you have not yet read (some will be posted soon if you click and are returned here, come back soon when the article will be posted):

The foundation article is: Millennials Are Buying Homes Near The Beach: Buy Yours Now

Budget Calculator and planner: Millennials Need This Now – You need to know what these required programs mean for those putting less than 20% down. This article explains your choices and what each means to the cost of your new home.

23 easy ways Millennials can improve their credit scores: 2023 it’s time to get that credit score higher. This article goes into all things credit reports and credit scores to help you pay the lowest interest rate possible. Use our tools and learn how you can keep your score high and improve it if it’s low.

The Homeowner’s Insurance Puzzle Made Simple for Millennials 2023 You need this information to make informed decisions about your homeowner’s insurance policy. Without a policy, there is no mortgage. You can overpay for coverage that others will offer for a lower price. When should you claim for damage, theft, etc.?

Credit Cards – How to get the most out of credit cards and manage them to your benefit.

The best free mortgage costs calculator – This article explains closing costs in detail including an embedded mortgage closing costs calculator. It’s a must-read to complete your financial education.

Mortgage Insurance – You need to know what these required programs mean for those putting less than 20% down. This article explains your choices and what each means to the cost of your new home.

The best mortgage loan guide for Millennials: Start now 2023– This article goes through an actual loan application so you can learn the process and how best to complete the form.

Millennials: How to find your first house in 2023 One of our longer articles goes through the entire process from locating a real estate agent to making the offer and the many steps that happen after the offer is accepted. Read this article after you have read all of the above articles because now you will be ready for the process.

This process takes from sixty to ninety days from the time you are ready to buy until you have the key. It’s an intense period that requires your complete attention and focuses on details. It’s also the most exciting part of the process. Finding that dream home may be a fast or slow process depending on a wide variety of factors discussed in this article.

We take you through each detail and show you most of the forms you will be required to sign during the process. Start working on those hand exercises, your signing hand is about to get busy.

Logan-Anderson Gulf Coastal Realtors is here to help you. If you are eventually looking for an affordable house in an affordable market, please go to our leading site LoganAndersonLLC.com where you can look at homes for sale. The Mississippi Gulf Coast is one of the most affordable home markets in the country. Read more about the area at RetireCoast.com