Last updated on March 3rd, 2023 at 06:23 pm

Last Updated on March 3, 2023 by

You are a Millennial in the process of buying a house. It’s time to obtain a homeowners insurance policy. Where do you start? What’s the actual cash value? And how much do I need for medical bills? The homeowner’s insurance puzzle for Millennials was made simple in 2023. If you are confused, join the club. Buying a homeowners policy is like listing to metal grating on metal.

When you receive the final printed package and I do mean package (20-40 pages), good luck reading it. This article will enlighten you to the point that you should be able to understand everything you need to know about home insurance coverage.

Before I dive into this topic, you should know that this article is one in our Millennial Financial Resources Series designed to educate Millennials about financial issues. One of our goals is to help any Millennial who wants to buy a house to succeed. You will find links to our series of articles at the end of the article.

What is a standard homeowners insurance policy?

Most people just want what some call “standard homeowners insurance policies” to close their purchase. I can tell you from experience with buyer clients that during the purchase period, everything is about getting paperwork done. Buyers are looking for that homeowner’s insurance premium to plug into their costs. There have been times when due to the debt-to-income ratio, the monthly premium that was quoted pushed them outside of the ratio.

This happened to me on a purchase. I went back to the insurance agent and asked if we could cut out some coverage. He came back with some lower coverages that would satisfy mortgage lenders and that lowered the price. I was back inside the ratio. After the property closed, I revised the policy and went back to the coverages that I wanted. This is part of the homeowner’s insurance puzzle made simple for millennials in 2022.

I am returning to my point about the jigsaw puzzle of homeowner’s insurance. That package I referred to above is a collection of pages that usually explain what is not covered and the few items that are.

Start with the first policy declaration page which summarizes coverages and essentially the “book” of pages starts chipping away at the first page.

Your mortgage company will require minimal coverage

Don’t misunderstand me, you do need enough coverage to both satisfy the mortgage company’s requirements and your own needs. I have made one claim in my life against a homeowners policy. Just one but that claim saved me over $20,000.

I encourage everyone to have a homeowners insurance policy on their property. All of my properties are insured. There are far too many perils today other than just the weather. Consider if you owned a house in a riot area and it was destroyed. How about having your house vandalized because of the way you voted? Years ago no one would have considered having coverage for any of these “modern” perils.

This article will focus on what some call the standard homeowner’s policy. This means that the coverages are typical for most but not all homes. Special perils are added when needed e.g. wind coverage. Sorry about not sharing some of the book pages with you, it appears they are all copyrighted. The Dwelling quote is free for me to share and so I have done it below.

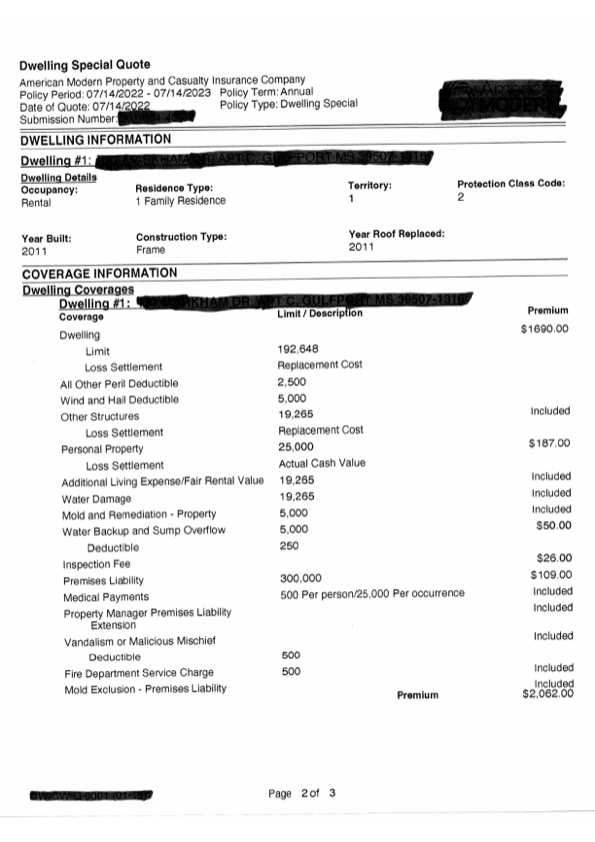

The Dwelling Special Quote

Let’s start your education process start with the “Dwelling Special Quote” or “Policy Declaration Page”.

These are typically one or two pages (see our example above) that as I mentioned above, summarize policy limits. Categories include but are not limited to personal property coverage, water damage, bodily injury, and more. Of course, the primary item is dwelling coverage which is the big number at the top.

For more clarity, I have included a YouTube video that goes through every line in our sample. Feel free to play it to supplement this article.

Insurance companies vary in their internal policies regarding the coverage limit. The insurance industry standard if there is such a thing is to list the limit as the cost to rebuild your damaged property. This limit is their “liability limit” which means they will pay no more than the stated amount.

In the case of our example, the limit is $192,648. Often, the limit listed is higher than the amount you paid for the property.

Why is the dwelling limit more than I bought the house for?

New homeowners often puzzle about the dwelling limit and ask why the amount is so much higher than what they paid for their home. Insurance carriers factor in the cost of rebuilding not what you paid for the property. As of this writing, the rebuild cost is generally around $200 per square foot. The limit is very often higher and in some cases much higher than you would expect.

Your lender may require a specific amount to protect their interest. I know, before I understood, I often argued with the agents about the limit amount. The first thing I would say is “the dirt does not burn down”. Please understand, that it is possible to be overinsured on the limit. Your agent uses the tools provided to determine the rebuild cost in your area.

The mortgage documents will specify minimum coverages. They want their asset to be protected, there is no consideration for the borrower. When you get past this number, the other items are much easier to understand and are more negotiable.

At this point, I want to throw in the other part of the liability coverage, the loss settlement clause. The example indicates that the replacement cost coverage is the same as the limit. Now, what exactly does replacement cost coverage mean?

You want replacement cost coverage

Usually “replacement cost coverage” means replacing damaged property with materials of a like kind and quality without any depreciation deduction. Ok, now what does that mean? This is a good type of coverage because they must essentially rebuild your house to be as close as possible to the original without using cheap materials up to the dwelling limit. There is one other method that is often substituted for “replacement cost” and that’s “actual cash value”.

Actual cash value is often the cost to replace damaged property less depreciation or the property, fair market value, or the broad evidence rule. Most homeowner’s coverages are based upon replacement cost. Just because the policy declaration page indicates replacement cost does not mean there are no exclusions to this buried in the book of pages. The cost of your policy starts with the biggest cost and that is the dwelling limit which represents the majority of the cost.

If you live in an area with what is described as “peril” such as high wind, hail, or other perils, a line will be included for this coverage. Property insurance costs are based in large part on these other perils such as hurricanes, fires, tornadoes, floods, etc. Property damage is likely to occur as a result of these additional perils rather than a stove fire or broken window from a tree falling. Just so you know, flood insurance will not be part of your liability protection.

Flood coverage is not the same as water damage

Flood coverage is a separate policy issued by a private carrier or the government flood program. Your basic policy may cover water damage caused by a broken water line for example. Water damage must be specified in the policy. In this example, there is an item for “water damage” and “water back-up and sump overflow.

Before moving on, let’s discuss “deductibles” depending upon your policy, you may be responsible for paying deductibles before you receive the first dollar. For example, if there is a wind event e.g. a tornado that tears your roof up. The deductible on this sample is $5,000.

If the roof repair cost $6,000, you will receive $1,000 from the insurance company. Water backup in your house, after paying the $500 deductible they will pay the rest. Keep these deductibles in mind before you make a claim. Here is why.

Weigh the downside of filing a claim

I mentioned above that I have made only one claim against an insurance company in my lifetime. What I have not mentioned is that several of my properties have been damaged over the years. In every case, I weighed the potential downside of claiming the actual out-of-pocket cost of repairs. Know this, if you claim any insurance, it will cost you down the road.

Three things may happen. Your policy may be canceled for a variety of reasons quoted e.g. we no longer want the risk, we don’t serve the area any longer, etc. Your rate may increase upon renewal or it will go up the following year.

One of my properties suffered some wind damage. A large tree collapsed in the yard without causing damage but the tree had to be removed. This was a large undertaking and required equipment. The cost of repairs and tree removal was about $4,000. The reimbursement after the deductible would have been about $500.

A claim on your house stays on the C.L.U.E record for up to 7 years

Rather than see my rate go up the following year or worse having the policy note for non-renewal, I wrote off the $500 as a casualty loss. Without a doubt, I saved about $2,000 in annual rate increases as a result of not making the claim. Clue will record a claim made on your house for up to seven years. Any future home insurance policies will have factored this in without my knowledge.

Homeowner’s insurance puzzle made simple for millennials. You know, I looked through the policy and did not see any reference to the information I just provided. Funny how that happens. Part of that puzzle.

The cost of homeowners insurance factors in the history of claims you have filed. Just as your credit score will give you a lower insurance cost if that score is high, your record of no claims will help keep your future costs low. Millennial property owners must evaluate the future cost of filing a claim vs covering the cost out of pocket.

If the claim is justified and it makes economic sense for you, make it. Evaluate the pain you are willing to endure before calling your insurance agency. You may want to consider for example not calling if one of the coverages has a $500 deductible and the total cost is $600 for repairs. Do you want to trigger a claim for a $100 return?

About the C.L.U.E. report on claims

Did you know that you are on record for every claim you have made with an insurance company for auto or home issues? True, a system called C.L.U.E. is used by all insurance carriers to keep track of your claims. This is a personal issue, not tied specifically to a house or a car. If you make a claim it stays in their system for up to seven years.

Did you also know that your credit score affects the price of your policy? It does. The better your score the lower your homeowner’s insurance policy will be. Something to consider as they check during renewals as well.

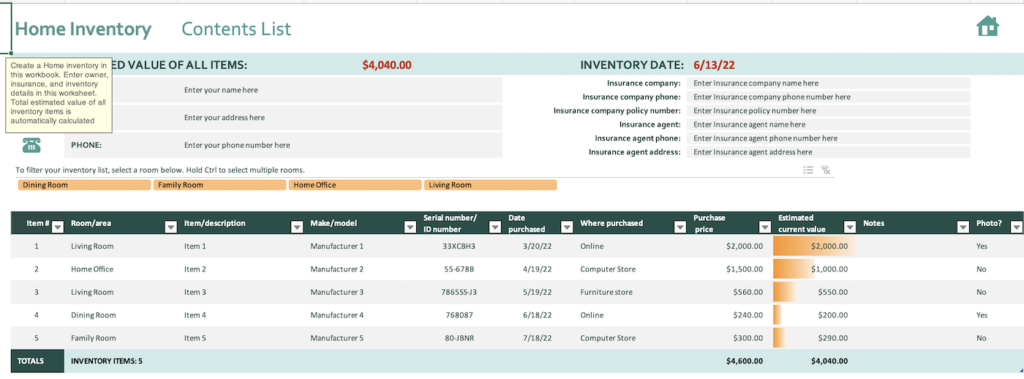

Back to that declaration page. Let’s go into personal property or contents insurance. It’s a good idea to make a list of items in your home. We have included an Excel file below found on the Microsoft Excel website. Download the file to your computer (found below the picture of the file below). Photograph any large items and expensive items. Record the purchase dates and amounts you paid. Doing this will speed up your claim. Insurance companies evaluate claims to detect attempted fraud. Never make a claim that is not accurate.

Inventory your property and determine the value

Select an amount for your policy. If you have a list you can add it up and develop a number. For your purposes, use a replacement cost number for everything. The cost of insurance for personal property is not unusually high. A typical three bedroom, 2 bathroom house of about 1,800 square feet will cost about $45,000 to fully furnish and that’s bed linens, couches, etc. If your house is larger and you have hobby items such as electronic equipment that value could reach $100,000. Remember the insurance company will only pay actual cash value.

It is possible to be overinsured in some categories. Personal property is one. You will never be paid more than the value of your property up to the total in the policy. No need to overpay for coverage you can not use. The same is true for the value of your house.

If the replacement cost is $250,000 then you do not need a $500,000 policy because you can never collect on the excess. Don’t pay for too much coverage at the same time do not pay so little that you have inadequate coverage.

It’s nice to have temporary housing covered during repairs

Additional living expenses. This is where you receive funds to offset the cost of temporary housing while yours is being repaired. The base price usually includes this coverage. You can have it increased as with anything in the policy if you are willing to pay extra for it.

Often water damage from a broken pipe for example will cause mold. Your policy should cover mold removal as well as clean-up of the water damage. Remember, this does not include a flood caused by a major disaster such as a hurricane.

Your insurance coverage includes a built-in inspection fee to check the damage done to your property. Be sure to allow the inspector full access to your property. In addition to an inspection should there be a claim, upon signing up for a policy there will be an initial inspection? A word about this first inspection. Check your house before the inspector comes out.

Before the initial inspection, fix safety issues

Fix any safety issues e.g. no fence around a pool, or electrical outlets without covers. This inspection will determine if you still have a policy. I know of situations where the insurance company terminated a policy after one month. The inspection revealed problems and the insurance company just walked away.

And yet another Homeowner’s insurance puzzle made simple for millennials.

The following items should be in good condition for an insurance inspector:

- The roof is in good condition, with no loose shingles or obvious signs of damage.

- The gutters are cleaned and in good condition

- The structure of the house is solid, with no large cracks in the foundation

- Elevated houses should not have standing water beneath

- Windows in good condition, no broken glass

- Entrance doors can be secure and opened from the inside in emergencies

- Check vegetation around the house, if it’s a dry area, remove it or fail

- Check the condition of trees that could fall on the house, trim limbs that overhang (if legal)

- Drainage of the property, be sure there is no ponding near the foundation

- The trash in the yard. If you like to accumulate things that others may think as trash, remove it.

- Gates must be securable

- Fencing and a gate must surround a swimming pool. Steps and decks must be safe

- Remove old autos, trucks, and boats. They may look abandoned

- Plumbing in the house must work, and all toilets, sinks, showers, etc. No leaking under the sink

- Check for mold including in the attic where a past water leak from the AC may have caused mold

- If there are obvious signs of past damage, paint or complete the repairs

- No locks on children’s doors could prevent an evacuation

- Stairs to the house or deck in good repair

- Exterior buildings locked to prevent entry to anyone without a key or combination

- Keep piles of fire logs well away from the house, check for termites

The above are just a few items on an insurance inspector’s list. As mentioned, I know of clients who lost their coverage after the inspection. In a few cases will the insurance carrier allow remediation and reinstatement? Don’t plan on it. You have one shot to get this right or lose your coverage.

Don’t lose your coverage over a bad inspection

If you lose your coverage, any new insurance company may see the reason why if the current company has uploaded information about the inspection. This can cause a delay in replacing coverage and the rate is likely to be higher.

Premises liability is usually included in a policy and is required by most mortgage companies. Your mortgage provider will have a minimum which is usually $300,000. This coverage is to protect you and the lender if someone gets hurt on your property. Believe me, this is a policy you need. Often this protection extends to items in your car parked in the driveway. It may also cover you for unexpected liability in other areas of your personal life.

The limits for premises or personal liability may be low. Considering that anyone can sue anyone for anything, this liability may be the only policy standing between you and financial ruin. A one-million-dollar policy may be more appropriate in higher-income areas.

Deductibles are typical for some coverage

Medical payments are to cover costs related to accidents for example. Medical coverage would cover the costs up to the limit if a neighbor fell and required medical care. Usually, the limit runs between $500 and $1,000 per person with a total per occurrence.

Property manager coverage listed is for rental property and does not apply to home ownership.

Vandalism or malicious mischief deductible is when someone does damage to your property as opposed to mother nature e.g. a rain storm. In this case, the first $500 is on you the remainder on the insurance company. Vandalism coverage is usually included in the base policy.

Misc coverages can include fire department call-out charges, first responder charges e.g. ambulance, etc. The base policy usually includes a variety of coverage types such as the first responder. Read the book to learn more about your specific exposure limits for each type.

If you want earthquake coverage, you must purchase it separately. The same is true for flood insurance.

About those policy renewals, listen up

Now that we have covered the basic insurance requirements and discussed each of them, it’s time to talk about other homeowners insurance issues. Your policy period is generally one year. Your insurance agent should notify you of upcoming renewal options.

You must pay attention at this time, about 30 days from the expiration date. Contact your agent and check for the renewal information. Don’t wait to be notified. If the renewal quote seems much higher than last year, it’s time to shop.

Check this item as another homeowner’s insurance puzzle made simple for millennials

It takes time to shop for insurance so start immediately. Independent agents usually offer more choices. Nail down that new policy and be sure that your insurance agent gets a copy of your mortgage company if they are making the payment for you. You should also send to them a copy of the renewal. Often the old carrier sends them a renewal and it is paid before you get the opportunity to shop. Notify your carrier you are shopping.

Don’t assume your policy will renew itself

Go to the insurance carrier’s website and use their proprietary communication system to send a copy of the renewal to them. You should receive an acknowledgment that your insurance provider has received your message. I am stressing this information because you never, never want a coverage gap. This is an excuse for non-renewal so is non-payment. If your mortgage company does not get notified in time they may miss the payment date. Please believe me from personal experience, these renewals rarely work without effort on your part.

Select an independent insurance agent

There are two types of insurance agents for homeowner’s policies. An agent that works for a single company such as Allstate and an agent who works for an independent brokerage. Both can produce homeowners’ insurance policies. The insurance products offered in a major metro area e.g. Las Vegas are similar between large companies and independent agents because the perils are similar.

When you live along the coast or in an area prone to flooding or tornadoes or snow storms, then the independent agent may be your best choice. The independent agent can find insurance companies that specialize in these “perils”. The major carriers do not offer “wind coverage” for example.

It’s not that the major insurance companies’ agents can not find separate wind coverage for you, they may be able to but it will almost always be more expensive than from an independent agent. If the house is newer and represents a lower risk, it’s easier to find coverage. Special peril areas e.g. along a cost have fewer insurance providers to choose from.

Where do you find a good agent?

Ask your real estate agent to refer someone. Why ask your real estate agent? Because they have one goal and that is to get you into that house as quickly and efficiently as possible. Your satisfaction is their only reason for being in the business. This means they know agents who will drag their feet on a quote and those who are fast and cost-effective.

Real estate agents work with insurance agents all the time and believe me, they know the good ones and the ones that should be avoided. There are also good agencies and poor agencies. As I mentioned above, you need to be notified when your policy comes up for renewal. A good agent will notify you.

A great agent will search for a lower-cost policy and then notify you with choices. Trust me, you want to work with a great agent and your real estate agent knows who they are. I often refer my client’s great agents. Here is an example. A policy just came up for renewal. The agent did a timely basis send the quote. I called another agent who cut the cost of renewal by over 40% and got it done in a week.

Buying that policy

Your policy will usually be written for a full year. Usually, your mortgage company will require impounds to pay for the policy. Every month as part of what you pay to the mortgage company is an amount for insurance. If factored correctly by the time the policy is due, the funds should have been accumulated.

Be prepared for your mortgage payment to increase after the first year. Not from interest or principal on fixed-interest policies but the higher cost of homeowner’s insurance and/or property taxes. Just expect your insurance policy to rise in cost each year. If you see it rise by a lot, contact your agent (who should have already contacted you). It’s time to search for a new policy with the same coverage for less.

On several occasions, I have paid the cost of the new policy with my credit card to get it in place on time. I talked a bit about that above. The insurance company eventually reimburses me.

I hope that this article is helpful to you. This is one of a series of articles written specifically to assist Millennials to succeed in life. Many parents of Millennials did not have the skills to teach their children some of these life skills. Hopefully, this series of articles will help you. To get the most out of them, please click on the other articles in the series that you have not yet read (some will be posted soon if you click and are returned here, come back soon when the article will be posted):

The foundation article is: Millennials Are Buying Homes Near The Beach: Buy Yours Now

Budget Calculator and planner: Millennials Need This Now – You need to know what these required programs mean for those putting less than 20% down. This article explains your choices and what each means to the cost of your new home.

23 easy ways Millennials can improve their credit scores: 2022 it’s time to get that credit score higher. This article goes into all things credit reports and credit scores to help you pay the lowest interest rate possible. Use our tools and learn how you can keep your score high and improve it if it’s low.

The Homeowner’s Insurance Puzzle Made Simple for Millennials 2022 You need this information to make informed decisions about your homeowner’s insurance policy. Without a policy, there is no mortgage. You can overpay for coverage that others will offer for a lower price. When should you claim for damage, theft, etc.?

Credit Cards – How to get the most out of credit cards and manage them to your benefit.

Mortgage Insurance – You need to know what these required programs mean for those putting less than 20% down. This article explains your choices and what each means to the cost of your new home.

The best mortgage loan guide for Millennials: Start now 2022– This article goes through an actual loan application so you can learn the process and how best to complete the form.

Millennials: How to find your first house in 2022 One of our longer articles goes through the entire process from locating a real estate agent to making the offer and the many steps that happen after the offer is accepted. Read this article after you have read all of the above articles because now you will be ready for the process.

This process takes from sixty to ninety days from the time you are ready to buy until you have the key. It’s an intense period that requires your complete attention and focuses on details. It’s also the most exciting part of the process. Finding that dream home may be a fast or slow process depending on a wide variety of factors discussed in this article.

We take you through each detail and show you most of the forms you will be required to sign during the process. Start working on those hand exercises, your signing hand is about to get busy.

Logan-Anderson Gulf Coastal Realtors is here to help you. If you are eventually looking for an affordable house in an affordable market, please go to our leading site LoganAndersonLLC.com where you can look at homes for sale. The Mississippi Gulf Coast is one of the most affordable home markets in the country. Read more about the area at RetireCoast.com

Register below to be notified of new blog articles.

Podcast

Note: We are not insurance agents and the information provided is for your use in searching for a good agent and insurance coverage. If you use any of the information above you do so at your own risk. If this article offends anyone in the insurance industry because it is inaccurate, please leave comments and we will consider them for changes to our article.